California School Bonds on the November 2020 Ballot: Are they equitable?

In each California election, there are sure to be school bonds on local ballots across the state. November 3, 2020 is no different: 55 school districts have general obligation (G.O.) bonds for school facilities revenue going before voters. Two districts – Gonzales USD in Monterey County and River Delta Joint Union SD in Sacramento County – each have 2 bonds before voters. In total, there is just under $12 billion in local bond authority going before voters across the state to modernize and construct public school facilities.

In our 2018 study for Getting Down to Facts II, we found wide disparities in school facility funding from district to district in California. Our analysis of 20 years of state and local funding found concerning patterns of inequitable access to school facility funding that are systematically related to school district property wealth, household income, and students’ backgrounds. While state funding through the School Facility Program (SFP) does seem to help very low-wealth districts with their facility needs, it has done little to lessen overall statewide disparities. As a result, we noted, California’s system of school facility finance is relatively regressive.

The evidence from the 69 G.O. bonds placed on local ballots by 66 school districts in the November 2020 election reveals that the long-standing patterns of inequity in public school facility funding in California remain strong.

The November 2020 bond authority proposals vary greatly from district to district. The smallest one proposes $2m (Sunnyside Union Elementary SD in Tulare County), while the largest is asking for $7b (Los Angeles USD). These amounts also vary greatly by enrollment: the smallest is just $318 per student (Dehesa Elementary SD in San Diego County), while the largest is $85,950 per student (Sausalito-Marin City SD in Marin County). On average, the ask is $13,818 per student in this election.

Let’s take a look at the relationship between local bond funds per student proposed on local ballots in November 2020 and 3 key local characteristics:

- local assessed property value in the district

- median household income

- student disadvantage as measured by the unduplicated pupil percentage enrolled in the school district

Do wealthier and more advantaged school districts tap more or less in local funds for their school facilities?

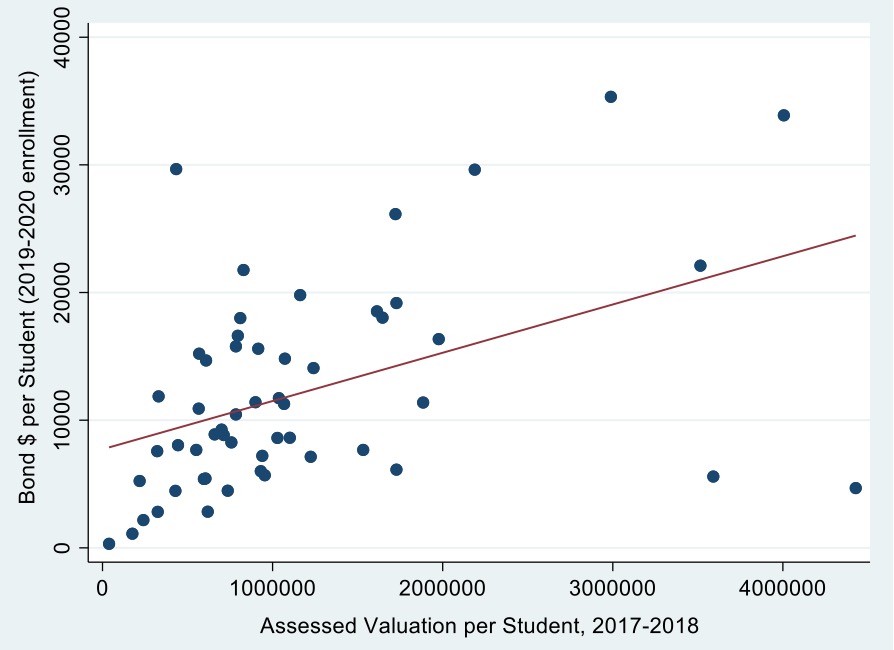

Local bonds and property values. Overwhelmingly, districts with higher local property values proposed more money per student in new bond authority. There is a strong positive correlation between bond dollars per student and local property values for all bonds proposed in November 2020, as the chart below shows

Note: Graph excludes two observations above $40,000 for better visualization.

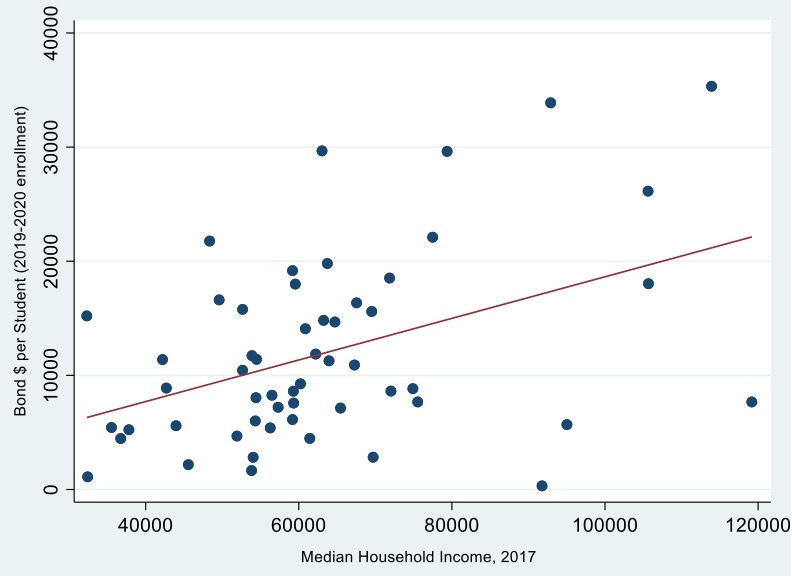

Local bonds and median household income. Overwhelmingly, school districts in wealthier communities proposed more money per student in new bond authority as is shown by the positive relationship between bond dollars proposed and median household income in November 2020, as the chart below shows.

Note: Graph excludes two observations above $40,000 for better visualization.

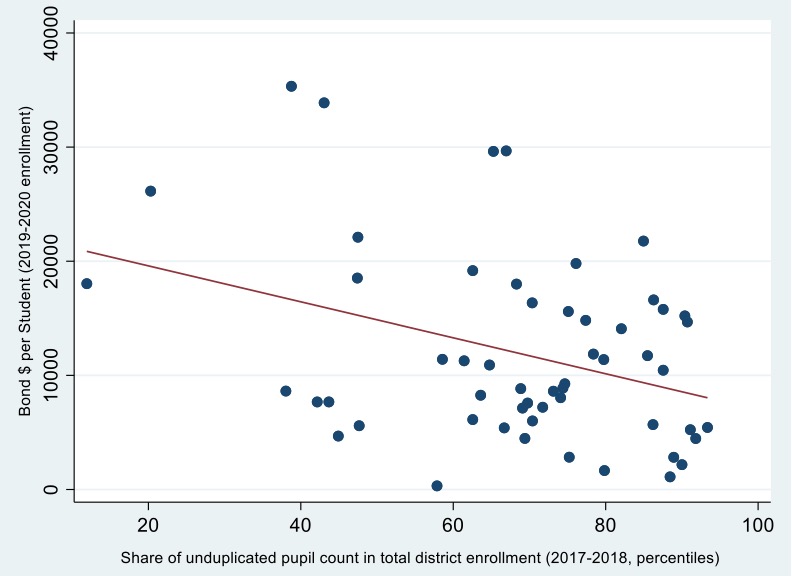

Local bonds and student disadvantage. Overwhelmingly, districts with higher shares of disadvantaged students proposed less money per student in new bond authority, as the graph below shows. This is showin the graph below illustrating the strong negative correlation between bond dollars per student and the district’s share of disadvantaged (“unduplicated”) students in November 2020.

Note: Graph excludes two observations above $40,000 for better visualization.

What these charts show is a continuation of the long-standing school facility funding inequities seen across California, as we found in our Getting Down to Facts study for the years 1998-2017.

Another metric to consider: bond dollars per student compared to student poverty as measured by the percentage of students in a school district qualifying for free/reduced price meals (FRPM). Wealthier districts (with FRPM below 50%) average twice as much per student as low-wealth districts (with FRPM above 50%): $22,548 per student compared to $10,976 per student.

State lawmakers tried recently to make some improvements to this persisten inequity in public education finance…but to no avail. Proposition 13 (2020), the “Public Preschool, K-12, and College Health and Safety Bond Act of 2020,” was placed on the March 3, 2020 statewide ballot. If passed, it would have authorized the issuance of $15 billion in bonds to finance capital improvements for public and charter schools statewide ($9 billion to improve K-12 school facilities and $6 billion for public universities and community colleges). The proposition included some equity-promoting reforms, including a new project prioritization system and an increase in the ability of low-wealth districts to quality for additional state funds. However, voters soundly rejected the proposition.

Proposition 13 (2020) only got 47% support at the polls. Despite having widespread support from state officials including Governor Newsom, Proposition 13 (2020) is the first statewide school bond to be defeated in 25 years.

So, for now at least, there is no state funding for public school facilities in California. A key role for state funding is to make up the gaps for lower-wealth school districts. Local school districts must go it alone to raise dollars for their facility projects.

And trudge forward they will.